European Tax Law Volume 2 - Studenteneditie

Indirect Taxation

Samenvatting

The student edition of this renowned handbook covers the harmonization of indirect taxes and discusses the main indirect taxes in the EU: customs law, VAT, excise duties, energy taxation and environmental taxation. The in-depth yet accessible approach to the subject matter allows students to deepen their understanding of indirect taxes in the EU.

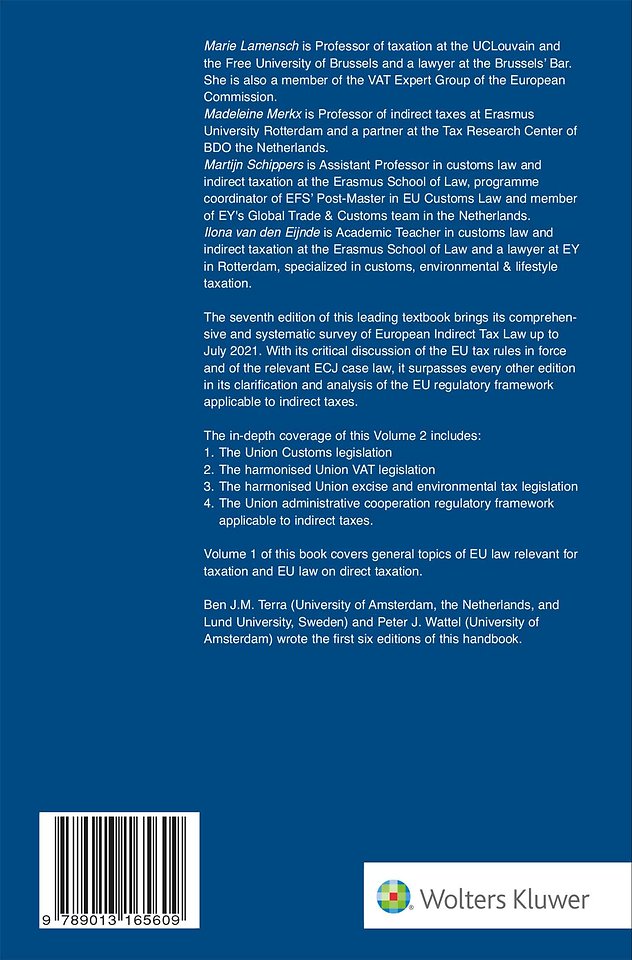

European Tax Law Volume 2 Studenteneditie provides students with a state-of-the-art yet highly accessible textbook on topics such as harmonization of indirect taxation, as well as the main indirect taxes in the EU: customs law, VAT, excise duties, energy taxation and environmental taxation. Where similar publications tend to adopt a narrow focus on a single indirect tax, this book enables the student to gain a full understanding of the most important indirect taxes in the EU. The 7th edition of this leading textbook brings its comprehensive and systematic survey of European Indirect Tax Law up to July 2021.

The volume is divided in four chapters, as follows:

- The Union Customs Code

- The Recast VAT Directive

- Excises and Energy taxation Directives

- Administrative cooperation in the field of indirect taxes

European Tax Law Volume 2 has been brought completely up to date with developments in case law and legislation. With its critical discussion of the EU tax rules in force and of the relevant ECJ case law, it surpasses every other edition in its clarification and analysis of the EU regulatory framework applicable to indirect taxes.

The in-depth yet accessible overview of indirect taxes in the EU makes this title the textbook of choice among students – no background or previous knowledge of indirect taxes is required.

Trefwoorden

Specificaties

Inhoudsopgave

Introduction / XIII

CHAPTER 1

The Union Customs Code / 1

Update and elaboration by Martijn Schippers

1.1 Introduction / 1

1.2 Legal sources / 2

1.2.1 The international legal (customs) framework / 2

1.2.2 The EU Customs Union / 3

1.3 General Provisions (Titles I and IX) / 4

1.3.1 The General Provisions of Title I / 4

1.3.2 Final Provisions / 9

1.4 Methods of Levying Duties (Titles II and III) / 10

1.4.1 Customs Debt and Guarantees / 11

1.4.2 Factors on the basis of which import duties are applied / 18

1.5 The System of Formalities and Supervision (Titles IV, V, VI, VII and VIII) / 36

1.5.1 Entry of Goods (Title IV) / 36

1.5.2 Customs Status, Customs Procedure, Verification, Release and Disposal of Goods (Title V) / 39

1.5.3 Release for Free Circulation (Title VI) / 43

1.5.4 Special Procedure (Title VII) / 45

1.5.5 Export and re-export (Title VIII) / 55

CHAPTER 2

Value Added Tax – the Recast VAT Directive / 57

Update and elaboration by Marie Lamensch and Madeleine Merkx

2.1 Introduction / 57

2.2 Subject Matter / 58

2.3 Scope / 61

2.4 Territorial Application / 61

2.5 Taxable Persons / 62

2.5.1 Introduction / 62

2.5.2 Any person / 62

2.5.3 Economic activity / 63

2.5.4 Continuing basis / 65

2.5.5 Independence / 65

2.5.6 Holding companies and share dealings / 66

2.5.7 Public bodies / 67

2.6 Taxable Transactions / 68

2.6.1 Supply of goods / 68

2.6.2 Intra-Community supplies / 73

2.6.3 Supply of services / 74

2.6.4 Importation of goods / 77

2.6.5 Vouchers – provisions common to supply of good and service / 77

2.6.6 New Means of Transport / 77

2.7 Place of Taxable Transactions / 78

2.7.1 Place of Supply of Goods / 79

2.7.2 Place of Intra-Community Acquisition of Goods / 81

2.7.3 Place of Supply of Services / 83

2.7.4 Place of Importation / 92

2.8 Chargeable Event and Chargeability of Tax / 93

2.8.1 Goods and services / 93

2.8.2 Intra-community acquisitions / 96

2.8.3 Imports / 96

2.9 Taxable Amount / 97

2.10 Rates / 101

2.11 Exemptions / 103

2.11.1 Exemptions without the Right to Deduction / 103

2.11.2 Exemptions Relating to Intra-Community Transactions / 116

2.11.3 Exemptions on Importation / 118

2.11.4 Exemptions on Exportation / 119

2.11.5 Exemptions Related to International Transport / 119

2.11.6 Exemptions Relating to Certain Transactions Treated as Exports / 120

2.11.7 Exemptions for the Supply of Services by Intermediaries / 120

2.11.8 Exemptions for Transactions Relating to International Trade / 121

2.12 Deductions / 123

2.12.1 Preliminary remarks / 123

2.12.2 Origin and Scope of Right of Deduction / 126

2.12.3 Refunds / 130

2.12.4 Proportional Deduction / 132

2.12.5 Rules Governing the Exercise of the Right of Deduction / 134

2.12.6 Adjustment of Deductions / 137

2.12.7 Private Use / 139

2.12.8 Deductions and Shares and Dividends / 140

2.12.9 Fraud and abusive practices / 148

2.13 Obligations of Taxable Persons and Certain Non-Taxable Persons / 152

2.13.1 Obligation to Pay / 152

2.13.2 Identification / 157

2.13.3 Invoicing / 158

2.13.4 Accounting / 167

2.13.5 Returns / 167

2.13.6 Recapitulative Statements / 168

2.13.7 Other Provisions / 169

2.13.8 Obligations in Respect of Imports / 169

2.14 Special Schemes / 170

2.14.1 Small and Medium-Sized Enterprises / 170

2.14.2 Farmers / 171

2.14.3 Travel Agents / 172

2.14.4 Second-Hand Goods, Works of Art, Collectors’ Items and Antiques / 173

2.14.5 Investment Gold / 174

2.14.6 Special schemes for reporting and remitting VAT by non-established businesses / 174

2.15 Derogations / 178

2.15.1 Derogations Applying until the Adoption of Definitive Arrangements / 178

2.15.2 Derogations Subject to Authorisation / 179

2.16 Miscellaneous / 180

2.16.1 Implementing Measures / 180

2.16.2 VAT Committee / 181

2.16.3 Conversion Rates / 184

2.16.4 Taxes Not to Be Characterised as Turnover Taxes / 184

2.17 Final Provisions / 185

2.17.1 Transitional Arrangements and Transitional Measures / 185

2.17.2 Transposition and Entry into Force / 186

2.18 Final words on the ECJ case law / 187

CHAPTER 3

Excises and Energy Taxation / 189

Update and elaboration by Ilona van den Eijnde

3.1 Introduction / 189

3.2 The Recast General Arrangements Directive / 193

3.2.1 General Provisions / 193

3.2.2 Taxable event, Time and place of chargeability, Irregularities during movement under duty suspension, Reimbursement, Remission, Exemption / 206

3.2.3 Production, Processing, Holding and Storage / 221

3.2.4 Movement of Excise Goods under a Suspension Arrangement / 222

3.2.5 Movement and Taxation of Excise Goods after Release for Consumption / 228

3.2.6 Miscellaneous / 234

3.2.7 Exercise of the Delegation and Committee on Excise Duty / 237

3.2.8 Reporting and Transitional and Final Provisions / 237

3.3 The ECMS Regulation / 238

3.3.1 General Provisions / 238

3.3.2 Implementing Provisions / 239

3.4 Mineral Oils / 250

3.4.1 The Original Rules with Regard to Mineral Oils / 250

3.4.2 The Rates on Mineral Oils / 252

3.5 Alcohol and Alcoholic Beverages / 253

3.5.1 Beer / 254

3.5.2 Wine / 255

3.5.3 Fermented Beverages other than Wine and Beer / 257

3.5.4 Intermediate Products / 258

3.5.5 Ethyl Alcohol / 258

3.6 Tobacco / 259

3.6.1 Definitions / 260

3.6.2 Provisions Applicable to Cigarettes / 261

3.6.3 Provisions Applicable to Manufactured Tobacco other than Cigarettes / 263

3.6.4 Determination of the Maximum Retail Selling Price of Manufactured Tobacco, Collection of Excise Duty, Exemptions and Refunds / 265

3.6.5 Final Provisions / 266

3.7 Environmental Taxation / 267

3.7.1 Introduction: VAT adjustments to reach environmental objectives / 267

3.7.2 Car Registration and Circulation Tax / 273

3.7.3 Plastic Tax / 278

3.8 The 2003 Directive on Energy Taxation / 279

3.8.1 The Scope / 280

3.8.2 Levels of Taxation / 282

3.8.3 Exemptions, Reductions and Tax Refunds / 286

3.8.4 Holding and Movement of Products / 291

3.8.5 Chargeable Event and Chargeability / 291

3.8.6 Final Provisions / 293

CHAPTER 4

Administrative Cooperation in the field of indirect taxes / 295

Update by Marie Lamensch and Madeleine Merkx

4.1 Legal Basis: ‘Internal Market’ or ‘Fiscal’ provisions? / 295

4.2 The Recovery Assistance Directive (applicable for direct and indirect taxes) / 296

4.2.1 History, Main Features, Scope / 296

4.2.2 Types of Recovery Assistance / 299

4.2.3 Limitations on the Obligations to Assist; National Treatment; (No) Preference / 300

4.2.4 Miscellaneous / 301

4.2.5 Evaluation of the RAD / 302

4.3 Trade Monitoring Provisions / 303

4.4 Administrative Cooperation and Combating Fraud in the Field of VAT / 304

4.4.1 Within the EU / 304

4.4.2 With third countries / 317

4.5 Administrative Cooperation in the Field of Excise Duties / 318

4.6 Administrative Cooperation in the Field of Customs Duties / 319

ANNEX I - Customs, VAT and excise legislation: territorial application / 323

Index / 327

Anderen die dit boek kochten, kochten ook

-

E. Bakker€ 49,00

E. Bakker€ 49,00 -

F.G.H. Kristen€ 79,95

-

Willie Elferink€ 59,95

-

Vina Wijkhuijs€ 49,95

-

René Repasi€ 46,00

-

Wim Van de Voorde€ 85,00

Net verschenen

Rubrieken

- aanbestedingsrecht

- aansprakelijkheids- en verzekeringsrecht

- accountancy

- algemeen juridisch

- arbeidsrecht

- bank- en effectenrecht

- bestuursrecht

- bouwrecht

- burgerlijk recht en procesrecht

- europees-internationaal recht

- fiscaal recht

- gezondheidsrecht

- insolventierecht

- intellectuele eigendom en ict-recht

- management

- mens en maatschappij

- milieu- en omgevingsrecht

- notarieel recht

- ondernemingsrecht

- pensioenrecht

- personen- en familierecht

- sociale zekerheidsrecht

- staatsrecht

- strafrecht en criminologie

- vastgoed- en huurrecht

- vreemdelingenrecht