Terra/Wattel European Tax Law - Volume 1 - Student edition

General Topics and Direct Taxation

Samenvatting

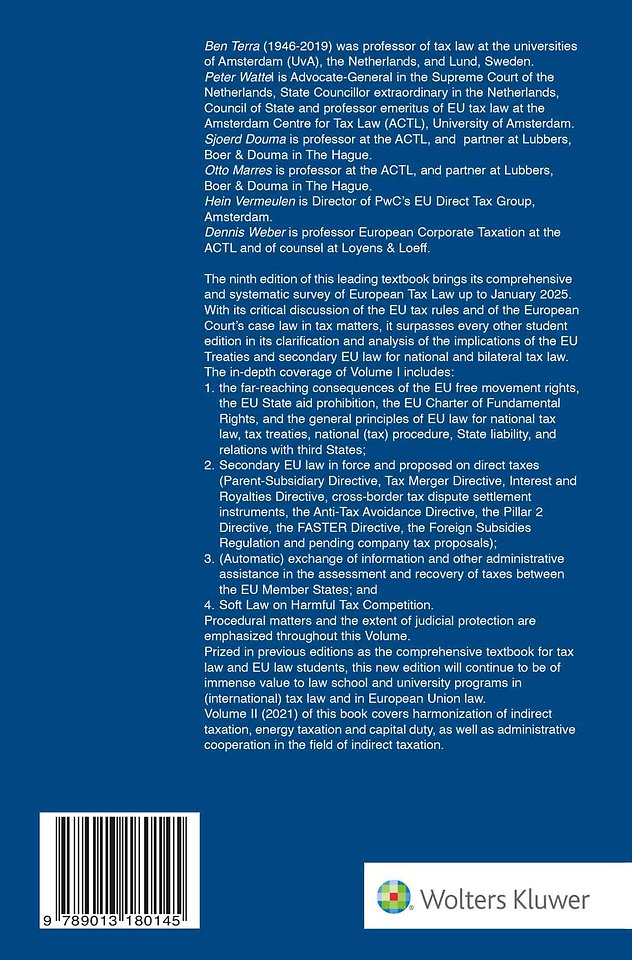

The ninth edition of this highly acclaimed book offers a comprehensive and systematic survey of European Tax Law up to January 2025. With its critical discussion of the EU tax rules in force and of the EU Court’s case law in tax matters, it surpasses every other publication on European tax law.

The Student Edition of European Tax Law thoroughly covers European Tax Law up to January 2025. Its previous editions have been praised as the comprehensive book on EU tax law for practitioners, policy makers, the judiciary and academics. This new ninth edition builds upon the series legacy and will continue to be of immense value as a reference work. The title surpasses every other publication in its clarification and analysis of the implications of the EU Treaties and secondary EU law for national and bilateral tax law.

This is the first volume of European Tax Law, covering a broad range of topics on direct taxation. The reader will gain insight into issues such as:

1. The far-reaching consequences of the EU free movement rights, the EU State aid prohibition, the EU Charter of Fundamental Rights, and the general principles of EU law for national tax law, tax treaties, national (tax) procedure, State liability, and relations with third States.

2. Secondary EU law in force and proposed on direct taxes (Parent-Subsidiary Directive, Tax Merger Directive, Interest and Royalties Directive, cross-border tax dispute settlement instruments, the Anti-Tax Avoidance Directive, the Pillar 2 Directive, the FASTER Directive, the Foreign Subsidies Regulation and pending company tax proposals.

3. (Automatic) exchange of information and other administrative assistance in the assessment and recovery of taxes between the EU Member States.

4. Soft Law on Harmful Tax Competition.

Volume II of this book covers harmonization of indirect taxation, energy taxation and capital duty, as well as administrative cooperation in the field of indirect taxation.

Trefwoorden

Specificaties

Anderen die dit boek kochten, kochten ook

-

Sjoerd Douma€ 29,00

Sjoerd Douma€ 29,00 -

Sjoerd Douma€ 118,74

-

Sjoerd Douma€ 154,71

-

Sjoerd Douma€ 137,64

-

Steven Jellinghaus€ 101,21

-

Vina Wijkhuijs€ 49,95

")

Net verschenen

Rubrieken

- aanbestedingsrecht

- aansprakelijkheids- en verzekeringsrecht

- accountancy

- algemeen juridisch

- arbeidsrecht

- bank- en effectenrecht

- bestuursrecht

- bouwrecht

- burgerlijk recht en procesrecht

- europees-internationaal recht

- fiscaal recht

- gezondheidsrecht

- insolventierecht

- intellectuele eigendom en ict-recht

- management

- mens en maatschappij

- milieu- en omgevingsrecht

- notarieel recht

- ondernemingsrecht

- pensioenrecht

- personen- en familierecht

- sociale zekerheidsrecht

- staatsrecht

- strafrecht en criminologie

- vastgoed- en huurrecht

- vreemdelingenrecht